Emerging Trends In Infusion/IV Therapy

By Ali Arabnejad and Kamran Zamanian, iData Research

Infusion therapy, or intravenous therapy, which involves delivering fluids and medications directly into the bloodstream, is a widely used medical treatment for various diseases such as cancer, infections, and autoimmune disorders. The infusion therapy market in the United States is growing rapidly, driven by an aging population and the increasing prevalence of chronic diseases. In this article, we share macro trends as well as trends in infusion pumps, IV sets, needleless connectors, stopcocks, IV filters, and blood transfusion sets.

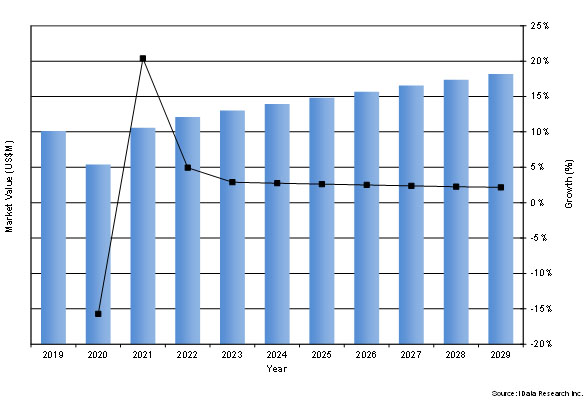

Figure 1: Market Value of Infusion Therapy Devices

Market Landscape, Size, And Trends

While established players like Baxter, Fresenius, B. Braun, ICU Medical, and Terumo dominate the market, startups and smaller companies are emerging as competitors. These smaller, more flexible competitors leverage innovative technologies and delivery systems, which make them more responsive to market changes and give them a competitive edge over larger rivals.

Growth in the market is expected due to the continuously rising demand in treatments for chronic diseases, along with the multiple requirements and uses of infusion therapy in treating the rising aging demographic of the baby boomer generation. As the market expands, new technologies and delivery systems are likely to emerge, accompanied by new players entering the competition. These developments are expected to improve patient outcomes and enhance the quality of life for individuals requiring infusion therapy.

According to new market research conducted by iData Research, the U.S. infusion therapy market size was valued at over $3.2 billion in 2022 and its CAGR is expected to be 2.5% over the forecasting period (2023–2029). This growth can be attributed to a number of factors, including the increasing prevalence of chronic diseases such as cancer and diabetes, the increase in the elderly population, and advancements in technology that have made infusion therapy more efficient and accessible.

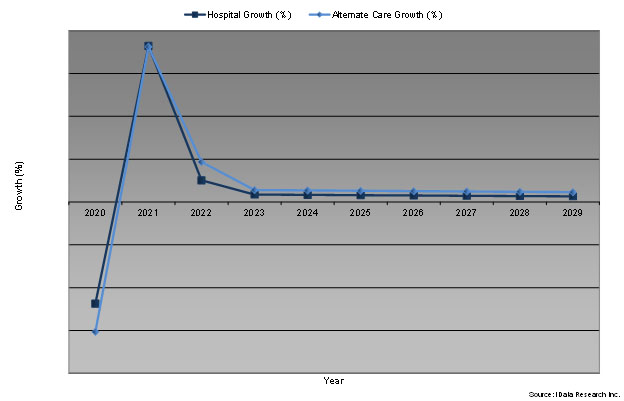

Figure 2: Hospital and Alternate Care Growth Rates in the Infusion Pump Market

The Shift Of Infusion Therapy Administration To Alternative Care Settings

The major trend that is driving growth in the U.S. infusion therapy market is the shift of procedures to alternative care settings such as specialty clinics, ambulatory surgery centers (ASCs), and home care settings. In the past, infusion therapy was primarily administered in hospitals or physicians’ offices. However, in recent years, there has been a shift toward alternative care settings, which offer a number of benefits to both patients and providers.

Specialty clinics offer an attractive option for infusion therapy patients because they often provide specialized care and expertise in the specific condition being treated. These clinics may offer a more comfortable and personalized setting, as well as shorter wait times and the ability to schedule appointments outside of traditional office hours. This can lead to improved patient satisfaction and better health outcomes.

Ambulatory surgery centers (ASCs) are another alternative care setting that has seen an increase in infusion therapy procedures. ASCs are equipped to handle more complex procedures than traditional outpatient clinics and offer patients the convenience of receiving infusion therapy without having to go to a hospital. Many ASCs are also able to offer lower costs for the same procedures performed in a hospital, making it an attractive option for both patients and providers.

Home care settings are also becoming a popular option for infusion therapy patients. Home infusion therapy allows patients to receive treatment in the comfort of their own homes, which can lead to increased patient satisfaction and a better adherence to treatment plans. Home infusion therapy also allows for more frequent monitoring of the patient's condition, which can lead to earlier detection of complications and improved patient outcomes.

Overall, the shift toward alternative care settings for infusion therapy procedures is a positive trend for the industry and for patients:

- Cost savings: Hospitals are typically the most expensive setting for infusion therapy, due to the high overhead costs associated with running a hospital. By contrast, specialty clinics and ASCs have lower overhead costs, which can translate into lower costs for patients. Home care settings can be even more cost-effective, as they eliminate the need for patients to travel to a medical facility for treatment.

- Convenience for patients: Specialty clinics and ASCs are often located in convenient locations, with ample parking and easy access for patients. Home care settings, of course, offer the ultimate in convenience, allowing patients to receive treatment in the comfort of their own homes.

- A higher level of personalized care: Hospitals are often crowded and busy, with little time for personalized attention from healthcare providers. By contrast, specialty clinics and ASCs are often smaller and more focused on individual patient needs. In the home, care providers can offer one-on-one attention to patients, ensuring that their needs are met and their treatment is administered safely and effectively.

The shift of infusion therapy procedures to alternative care settings has been driven in part by changes in reimbursement policies. In recent years, Medicare and private insurers have begun to reimburse providers for infusion therapy administered in non-hospital settings. This has made it more financially feasible for providers to offer infusion therapy in these settings, which has in turn led to an increase in demand for these services.

As the trend continues, we may see further innovations in delivery systems and technology to better facilitate the transition to these alternative care settings.

Trends And Growth Within Segments

Now, let's discuss the trends and growth factors within the segments of the infusion therapy market in more depth.

Infusion Pumps

Infusion pumps offer precise fluid and medication control and have evolved from the gravity-based drips of the 1960s to the compact, agile devices of today. Portable and wearable devices are a prominent trend, offering patient mobility and enabling home-based care. Integration with telehealth platforms is on the rise, allowing remote monitoring and timely interventions. Specialized infusion pumps tailored to unique treatments are expanding, ensuring safe medication delivery.

Despite challenges from the fluctuating availability of hospital beds amid the pandemic, the infusion pump market remains resilient. Anticipated growth is driven by patient-controlled analgesia (PCA), syringe, and electronic ambulatory pumps. While most segments' average selling prices are expected to remain stable, innovations in hardware and software will enhance device safety and efficiency, potentially impacting market average selling price (ASP).

Intravenous Sets

Intravenous (IV) sets can be in the form of primary sets, including pump and gravity sets; secondary sets for simultaneous dual fluid infusion; and extension sets for added length or specific features like filters or stopcocks. The IV sets market offers diverse configurations for specialized applications, such as oncology, with safety features and accessories like filters and flow control.

A significant trend in the IV sets market is the adoption of antimicrobial-coated sets, designed to mitigate the risk of infections associated with intravenous therapy, with a heightened focus on patient safety, especially in critical care and high-risk settings.

Another noteworthy trend is the increasing demand for customizable IV sets, allowing healthcare providers to tailor sets to specific needs, enhancing efficiency and reducing medication errors. Evolving regulatory standards ensure compliance, instilling confidence in the reliability and safety of IV sets.

The IV sets segment is poised for sustained growth. The adoption of antimicrobial-coated sets is expected to gain further traction as patient safety remains paramount. Customization options will continue to flourish.

Needleless Connectors

The needleless connectors (NLCs) segment plays a vital role as the interface between medical devices and intravenous access, ensuring safe and contamination-free administration of fluids and medications. This segment has witnessed significant acquisitions and consolidations among major players, expanding product portfolios and fostering innovation. Split septum connectors and mechanical valve connectors are the primary types, with mechanical valves gaining dominance in 2022 due to reduced blood reflux concerns.

NLCs are available as stand-alone products or integrated with IV extension sets; the majority were sold as integrated devices in 2022, offering convenience and time savings during IV starts. The market shares of stand-alone and integrated devices are expected to remain steady, with no conclusive evidence favoring one over the other in terms of patient outcomes, as well as their minimal cost differences. The U.S. NLC market includes antimicrobial and conventional non-antimicrobial devices, with the latter dominating in 2022 due to lower costs and extended disinfection duration for antimicrobial connectors. High costs and extended contact time constraints are expected to limit the growth of antimicrobial NLCs.

Closed-system transfer systems (CSTS), a subset of NLCs, are gaining prominence, enabling safe substance transfer while protecting healthcare workers. These trends reflect a commitment to patient safety and workplace security in healthcare.

The NLC segment is poised for continued growth as healthcare stakeholders prioritize patient safety, infection control, and the reduction of healthcare-associated infections. The ongoing trend of acquisitions and consolidations among industry leaders is expected to drive innovation and expand market reach. The integration of advanced infection prevention features and the adoption of closed-system transfer systems reaffirm the commitment to providing safe and effective intravenous access in diverse healthcare settings.

Stopcocks

Stopcocks are vital components in complex IV lines used in surgical and critical care scenarios, facilitating simultaneous medication infusions and fluid mixing. Sold as stand-alone add-ons, manifolds, or integrated with extension IV sets, they are typically constructed from translucent plastics and silicone to control bacterial formation. These devices come in various configurations (one-way, two-way, three-way, and four-way) with ergonomic handles and different arm handle colors for fluid distinction, diverse port designs (short nut, long nut, luer slip, and all-female ports), and additional features like port protection and color-coded caps. In the U.S. stand-alone IV-line stopcock market, four-way stopcocks are the largest segment, followed by three-way stopcocks, while one-way and two-way stopcocks have a smaller market share. The product mix is expected to remain relatively stable, with four-way stopcocks potentially experiencing slight growth.

The stopcock segment is poised for continued growth, driven by the pursuit of precision and safety in fluid control within the medical field. Ongoing innovations in design and materials are expected to enhance the performance and reliability of stopcocks.

IV Filters

Several influential trends are shaping the IV filter market and fueling its growth. One key trend is the development of specialized membranes within IV filters (typically featuring a 0.2-μm pore-type membrane for bacteria and a 1.2-μm "mesh" membrane for lipids), enabling precise particle removal tailored to specific filtration needs, such as eliminating bacteria, air microbubbles, or lipid clusters from intravenous solutions. This specialization enhances the effectiveness of IV filters, ultimately leading to better patient outcomes. Ongoing research and development efforts are expanding IV filter capabilities, with a focus on establishing the link between filtered solutions and improved patient recovery rates, reinforcing the importance of these devices in modern healthcare. IV filters are versatile, finding applications in various medical scenarios from standard medication filtration to specialized needs like blood transfusions and total parenteral nutrition (TPN), ensuring their indispensability in a wide range of medical treatments.

The IV filter segment is poised for continued growth as healthcare providers prioritize patient safety and treatment efficacy. Specialized membranes and ongoing research are expected to drive advancements in IV filter technology, improving their ability to filter a wide range of intravenous solutions effectively. As the evidence supporting the benefits of IV filters continues to mount, their significance in ensuring patient health and enhancing the quality of care delivered in healthcare settings will only grow.

Blood Transfusion Sets

Blood transfusion procedures rely on specialized IV sets with blood filters for safe and efficient blood and blood product transfer. These sets facilitate filtration, reducing microaggregates (20 to 200 µm) during the process, ensuring safe transfusions. Blood collection IV sets are designed with shorter lengths, IV bag connections, and thicker needles. In addition to filtration, IV tubing for blood administration requires filters (40 to 260 micron) and often features a dual-spiked configuration for testing.

There is a growing emphasis on incorporating warming technologies within transfusion equipment to enhance patient comfort and procedure efficiency, ensuring blood products are administered at the optimal temperature.

The U.S. market for blood transfusion sets comprises single-chamber and dual-chamber sets, with dual-chamber sets dominating the market due to their ability to deliver two medications simultaneously or sequentially in critical care settings, while single-chamber sets serve routine treatments in non-critical care settings.

The blood transfusion set segment is expected to maintain steady growth in the coming years, driven by the persistent demand for blood products and ongoing advancements in transfusion technology. The integration of warming technologies and the development of innovative transfusion equipment are poised to further improve the patient experience and the efficiency of blood transfusion procedures.

Challenges And Limiting Factors

While the U.S. infusion therapy market is expected to continue to grow in the coming years, the market also faces challenges. One of the biggest challenges is the shortage of trained healthcare professionals who are able to administer infusion therapy. This shortage is particularly acute in rural areas, where access to healthcare providers can be limited. Addressing this shortage will be critical to ensuring that patients are able to receive the infusion therapy they need in a timely and effective manner.

A more limiting factor for the infusion therapy market, from a medical device perspective, is the high cost of developing and producing new equipment. Medical device companies must invest significant resources in research and development to bring new products to market, as well as adhere to strict regulatory requirements. This can result in higher prices for infusion therapy equipment, which may limit access to care for some patients and put a strain on healthcare budgets. As a result, there is a growing need for collaboration and partnerships between medical device companies, healthcare providers, and payers to find ways to bring innovative and effective infusion therapy equipment to market at an affordable cost.

Closing Thoughts

In conclusion, the infusion therapy market in the United States is rapidly growing and it is expected to continue to do so due to factors such as the increasing prevalence of chronic diseases, the aging population, and advancements in technology. The shift toward alternative care settings is driving growth in the industry, providing greater convenience, cost savings, and personalized care for patients. However, challenges such as the shortage of trained healthcare professionals and the high cost of developing and producing new equipment remain. Overall, the infusion therapy market has a promising future as it continues to improve patient outcomes and the quality of life for those who require infusion therapy.

References

- O'Grady NP, Alexander M, Burns LA, et al. Guidelines for the Prevention of Intravascular Catheter-Related Infections. Clin Infect Dis. 2011;52(9):e162-93. doi: 10.1093/cid/cir257. PMID: 21460264.

- Diamantis P, Pimentel M, Karamanis K, Kontou P, Tsaroucha A. Infusion-related complications and their management in patients receiving home-based parenteral nutrition: a systematic review. Ther Clin Risk Manag. 2018;14:1113-1124. doi: 10.2147/TCRM.S165215. PMID: 29942160.

- Cohen S, Ernst FR. Economic burden of infusion therapy and challenges in improving value. Nat Rev Rheumatol. 2016;12(12):711-719. doi: 10.1038/nrrheum.2016.171. PMID: 27725632.

- Li Z, Hu J, He J, Sun J. Efficacy of intravenous immunoglobulin combined with plasmapheresis for the treatment of immune thrombocytopenia: a meta-analysis. Ther Apher Dial. 2019;23(5):416-423. doi: 10.1111/1744-9987.12851. PMID: 30729689.

- Sharma G, Sharma A, Kumar P, Sharma A, Rattan R. Extravasation injury during intravenous drug therapy: A literature review and institutional experience. Indian J Cancer. 2021;58(1):1-7. doi: 10.4103/ijc.IJC_60_20. PMID: 33753614.

About The Authors:

About The Authors:

Ali Arabnejad is a research analyst at iData Research, specializing in the medical device industry. He is responsible for spearheading syndicated research projects such as the Ear, Nose, and Throat Report series, as well as the Infusion Therapy Report series.

Kamran Zamanian, Ph.D., is CEO and founding partner of iData Research. He has spent over 20 years working in the market research industry with a dedication to the study of medical devices used in the health of patients all over the globe.

Kamran Zamanian, Ph.D., is CEO and founding partner of iData Research. He has spent over 20 years working in the market research industry with a dedication to the study of medical devices used in the health of patients all over the globe.