Growth Strategies Pushing The Next Wave Of Surgical Robotics

By Corinne Nawn, Ph.D., Back Bay Life Science Advisers

As we near the end of 2023, elective surgical procedures, one of the many victims of the COVID-19 pandemic, are recovering to near pre-2020 levels. As a result, several of the large cap medtech companies increased their 2023 revenue expectations. Within this context, robotic surgery is primed for an acceleration in activity – both in its clinical utilization as well as its strategic importance to the venture community and consolidators alike.

The market leader, Intuitive, was among the medtech players to increase full-year forecasts, citing 20%-22% year-over-year growth in procedures using its surgical robotic platform, DaVinci. Recently, Stryker attributed the double-digit growth of its orthopedic business line to the uptake of its Mako robot in hip and knee procedures. While only ~10% of surgical procedures worldwide are performed with robotic assistance, early commercial traction from first-generation robotic technologies bodes well for the space overall.

Given the significant opportunity to grow the overall market, the next wave of exciting robotic surgery innovations has caught the eye of medtech investors.

Funding Flow

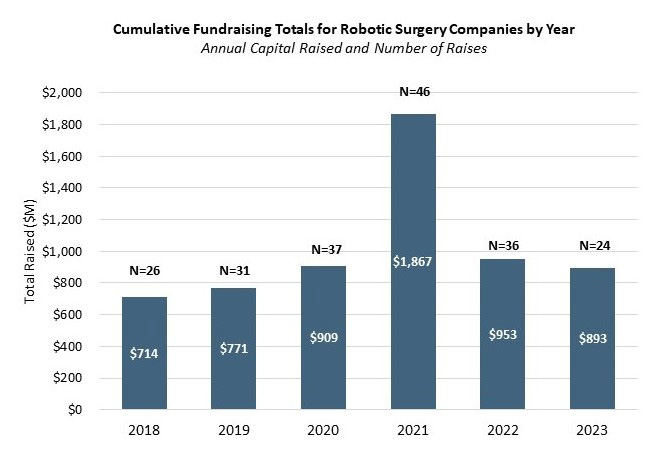

Figure 1: VC Financings of Robotic Surgery Companies by Year, January 2018-October 2023

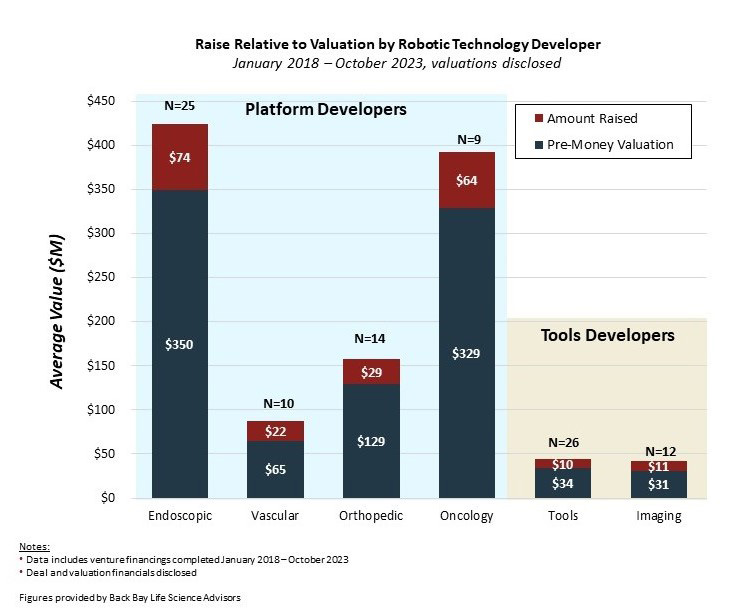

Since 2018, robotic surgery startups have raised almost $6 billion in venture capital over ~200 financings (Figure 1). Average raises were around $25 million, except for 2021 and 2023, which averaged around $40 million. Notably, despite the present challenging fundraising environment, deal volume for robotic surgical companies has remained strong and has even seen a 40% increase in average raise as companies mature in later stages of development. We assessed the funding dynamics for companies based on the core technology under development, namely whether they were platform developers or tools developers (Figure 2).

Platform developers are designing complete systems intended to be the predominant platform used for the surgical intervention. This category includes a broad a range of systems from large, stand-alone suites, such as the traditionally envisioned DaVinci where the surgeon operates remotely, to robotic assistant platforms that involve fewer components, such as Moon Surgical’s Maestro system, which work alongside the surgeon during the procedure. In contrast, tools developers are focused on developing adjunct technologies designed as add-on components for a robotic surgical suite – such as, for example, imaging or physical instrumentation tools to improve procedural capabilities or efficiencies. On average, platform developers commanded higher valuations compared to those developing surgical robotic tools (Figure 2).

As these companies have to pursue indication-based FDA approval, rather than more technically-oriented approvals (e.g., visualization markers, surgical instruments, etc.), this often leads to longer and more costly development timelines with clinical trials. Depending on the surgical application and complexity of the robotic system (e.g., stand-alone suite vs. robotic assistant platform), companies typically have to raise around $100 million to $300 million to achieve FDA approval.

Furthermore, platform developers also have to engage in significantly more market development activities, cultivating physician champions to serve as both development partners as well as early adopters for a successful launch. Especially with robotic surgery still being in its early stages of broad clinical practice, key opinion leaders play a critical role in driving ultimate adoption by conducting studies and presenting evidence on clinical and economic utility – thereby supporting the argument for adoption by other physicians as well as hospital systems.

On the other hand, tools developers have lower overall valuations but have a much more capital-efficient runway to achieve the same FDA-approval inflection point – raising ~10x less capital on average than platform developers. Since these companies are developing adjuncts to existing procedures, they are often able to streamline development with FDA approval based on predicate devices with objective measurement endpoints (e.g., validating imaging accuracy) rather than any clinically dependent outcomes. For example, Insight Medical Systems developed an augmented reality (AR) visualization system for orthopedic surgeries – raising only $11 million to achieve FDA approval and successfully complete ~200 cases in the U.S. before being acquired by Enovis in July 2022 (terms undisclosed).

Figure 2: VC Financings of Robotic Surgery Companies by Developer Type, January 2018-October 2023

Platform Development

While the first generation of robotic platforms offered the value of transitioning traditionally “open” procedures to minimally invasive ones, this next generation will have to be more creative in differentiation. Advancements in material science, motors, and actuating mechanisms are creating surgical robotics with greater degrees of freedom and flexibility, thereby enabling minimally invasive access to body areas previously inaccessible or requiring greater (open) surgical exposure. These innovations can continue to grow the overall market by expanding the number of procedures addressed robotically and reducing the overall cost of care with decreased recovery time.

For example, EndoQuest’s Flexible robotic system is designed to target surgical procedures through natural orifices (e.g., oral, umbilical, anal, vaginal) for scar-free or single-incision surgeries. Not only does their platform offer the potential to expand into unique applications, but it pushes the “decreased recovery” argument further with scar-free access. Another leading startup, Virtual Surgical, is tackling another critical unmet need within robotic surgery – addressing the cost of care by developing a modular platform that reduces the setup and turnover time within the OR, allowing for greater portability. With the capital acquisition costs and increasing number of surgical procedures moving to ambulatory surgical centers (ASCs), making robotic surgery more portable and cost efficient represents a key barrier to unlock greater market adoption.

Similarly, Moon Surgical is addressing the barrier to robotic adoption by developing a platform designed to integrate more closely into current surgical workflows. Its dual-armed robotic system takes on a similar role as the surgical assistant, thereby providing value to the surgeon as well as the hospital system by reducing the staffing needs in an OR. Furthermore, Moon is commercializing its recently 510k-cleared system with a unique subscription model to decrease the capital barrier and target institutions previously unable to justify the significant CapEx investment for robotic platforms such as DaVinci due to lower procedure volumes or budget limitations.

Tools Development

For tools developers, the market development activities focus on technological improvements as add-ons to the stand-alone robotic platforms. Thus, clinical differentiation depends on a company’s ability to partner with strategic players earlier to validate its value propositions as well as establish a “bolt-on” foundation for uptake.

An example of this is Osso VR, which has developed an AR solution to facilitate surgeon training on new robotic systems, a key point of friction for many platform developers in driving physician adoption. Consequently, Osso has established partnerships with several of the major robotic players in orthopedics, such as Stryker, Zimmer Biomet, and Smith+Nephew. eCential Robotics, a Grenoble-based tools developer, is developing an open 2D/3D imaging solution for robotically assisted bone surgeries and has been successful in securing multiple strategic partnerships with other spinal and orthopedic implant companies such as Spineart, ChoiceSpine, and Amplitude Surgical.

Improving intraoperative visualization represents a strong value proposition for the surgeon’s use, since the transition from open procedures to minimally invasive ones inherently limits their natural field of view. Especially given the strong influence surgeons have on product adoption, this perceived value translates to platform developers looking to win surgeons’ favorable opinions.

Implications For Strategy

From a corporate strategy perspective, startups with robotic surgery technologies should consider their relative appetite for “build to sustain” or “build to buy.” Companies developing platform technologies more often take a build to sustain approach, raising from venture investors as they develop toward FDA approval and considering an IPO to support commercialization.

Leading next-generation platform developers such as Stereotaxis, Asensus Surgical, and Vicarious Surgical have recently taken this pathway as they seek to leverage the capital markets as a continued source of funding for the capital-intensive process of manufacturing scale-up of the robotic systems as well as for a highly skilled salesforce to train and cultivate the early clinical and institution adopters.

Alternatively, tools developers can maintain a more capital-efficient development runway and tend to seek a build to buy pathway that is contingent upon partnership and incentivizing acquisitions. To this aim, these companies will need to strategically consider the trade-offs between being able to demonstrate early commercial traction without unnecessarily building out internal functions that would be redundant or conflicting with potential acquirors.

As an incumbent first-generation robotic system in the field, entertaining partnerships or acquisitions will be vital to maintain market position. Entrenched players have the advantage of having already overcome the initial barrier to institutional adoption but face the challenge of driving volumes for revenues. This can be achieved in several ways – optimizing procedural cost efficiencies for hospital value, augmenting technical capabilities to incentivize physician utilization, or expanding platform applications to access new patient populations. As tools and platform developers validate their technologies’ value propositions, consolidators should map these potential offerings across their own internal capabilities to evaluate where and how they want to build, buy, or partner to keep up in the rapidly accelerating robotic surgical market. As of midyear financial reports, 10 of the largest medtech players have over $1 billion in cash on hand, including historically active acquirers with robotic surgery portfolios, such as Medtronic, Stryker, and GE Healthcare. This dry powder adds another element likely to fuel the activity within the surgical robotics market.

About the Author:

Corinne Nawn, Ph.D., is a senior consultant at Back Bay Life Science Advisors. She supports strategic engagements by employing her scientific and engineering backgrounds across a range of therapeutic areas and technologies, particularly specializing in medical devices and digital technologies. Previously, she worked at the U.S. Army Institute of Surgical Research where she developed battlefield medical devices while pursuing her Ph.D. in biomedical engineering from the University of Texas at San Antonio and UT Health San Antonio. She also consulted for the city of San Antonio to develop a collaborative framework for industry, academic, and governmental entities to partner around military medical solutions. Before her work in Texas, she attended Worcester Polytechnic Institute where she majored in biomedical engineering and minored in computer science. Connect with the author at www.bblsa.com.

strategic engagements by employing her scientific and engineering backgrounds across a range of therapeutic areas and technologies, particularly specializing in medical devices and digital technologies. Previously, she worked at the U.S. Army Institute of Surgical Research where she developed battlefield medical devices while pursuing her Ph.D. in biomedical engineering from the University of Texas at San Antonio and UT Health San Antonio. She also consulted for the city of San Antonio to develop a collaborative framework for industry, academic, and governmental entities to partner around military medical solutions. Before her work in Texas, she attended Worcester Polytechnic Institute where she majored in biomedical engineering and minored in computer science. Connect with the author at www.bblsa.com.