Innovation Woes, Or: How I Learned To Stop Worrying And Love My Failed Device

By Alexander Marsolais, PhD, Sheryl Tang, MPH, and James Spencer, BSc

Viewed at a high level, a large proportion of the medical device market is commoditized (think bandages and IV bags). However, anyone who has attended a medical conference recently knows that there is a great deal of innovation going on, with exciting new technologies debuting across a wide range of product categories. Understanding how these technologies are differentiated from previous iterations allows us to forecast their likely impact on their respective markets.

Given the vast improvements to our collective health and life expectancies over the past several generations, we have become used to the idea that innovation in the healthcare space follows a sweeping upward trend towards ever better technology (and health outcomes). Considered in aggregate, it is certainly the case that innovations in medical technology have had a net positive impact on human health. However, the gritty reality of innovation in medical markets is that there are many misfires along the way, and the stakes for manufacturers are high.

This article focuses on two recent, high-profile examples of new technologies failing to meet expectations in their early development. In both examples, innovative ideas that were transformative in theory stumbled in their first real-world applications as part of high-profile clinical trials.

Neither idea has been entirely abandoned. Each technology remains the subject of active research and development, and both may yet transform their markets. The moral of these stories (and of innovation in healthcare, more generally) is that companies are right to temper excitement — about new technologies and acquisitions — with realism about the potential downsides of pursuing innovative ideas, particularly in the short term.

Bioresorbable Vascular Scaffolds

Myocardial infarction (commonly known as a heart attack) is caused by ruptured atherosclerotic plaques leading to flow-limiting blood clots in coronary arteries. Historically treated through coronary artery bypass graft (CABG) procedures, they now are commonly treated through percutaneous coronary intervention (PCI). During a typical PCI, an intravascular balloon is dilated inside of the occlusion to restore normal blood flow, after which a stent is placed to keep the vessel open.

While coronary stent manufacturers continue to innovate within the field of traditional metallic stents, the market has become commoditized over the past 10-15 years. Hence, there was considerable excitement when Abbott Vascular launched the Absorb. This device was a departure from standard metallic stents, which remain in the patient’s vasculature for the rest of their lives and can lead to complications years later, such as late in-stent restenosis. Termed a ‘bioresorbable vascular scaffold’ (BVS), the Absorb was designed to circumvent this issue by dissolving back into the body after the vessel has healed, preventing any chance of re-stenosis or other adverse events resultant of a foreign object remaining in the body.

Upon the device’s original launch, Abbott Vascular heavily marketed the Absorb as a new paradigm in PCI and pursued an aggressive commercialization strategy, particularly in Europe and Asia. However, the device was dogged by ambiguous or negative clinical results. Following some initial negative registry data, the randomized ABSORB II trial showed that patients who had an Absorb device implanted had a significantly higher rate of myocardial infarction post-implantation than patients who were treated with best-in-class drug-eluting metal stents (DES)10.

The ABSORB III trial was a further blow11, largely confirming the findings of the ABSORB II. The principal driver of Absorb’s failure to achieve positive trial outcomes appears to be the device’s large strut thickness (necessitated by the fact that it is made of a polymer and not a metallic alloy). The large strut thickness makes a BVS more difficult to deploy (into the narrowed arteries they are meant to treat), and increases the short-term risk of complications, such as stent thrombosis. Due to these results, the Absorb seldom achieved more than 1-5 percent of PCI procedure share, and Abbott Vascular shelved the product in September 2017.

This episode highlights a further pitfall to technological innovation that fails to deliver results — in addition to the expense and resources required to develop and trial a product that fails to deliver on its promise. Launching in late 2015, Boston Scientific’s newest metallic DES, the SYNERGY, had secured approximately 35 percent of the total U.S. market share by the end of 2016. While much of this share gain came at the expense of Boston Scientific’s legacy Promus PREMIER DES, the company was successful in taking share away from one of its main competitors (Medtronic), while cementing its lead over Abbott Vascular, the one-time market leader.

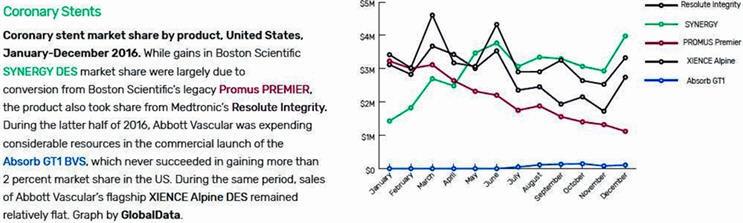

Coronary stent market share by product, United States, January-December 2016. While gains in Boston Scientific SYNERGY DES market share (dark blue) were largely due to conversion from Boston Scientific’s legacy Promus PREMIER (light blue), the product also took share from Medtronic’s Resolute Integrity (light green). During the latter half of 2016, Abbott Vascular was expending considerable resources in the commercial launch of the Absorb GT1 BVS (dark red), which never succeeded in gaining more than 2 percent market share in the US. During the same period, sales of Abbott Vascular’s flagship XIENCE Alpine DES (light red) remained relatively flat. Graph by GlobalData.

This success was based on the strength of the device’s intra-procedural advantages. These improvements — including its ease of deployment and its ‘trackability,’ or visibility in the fluoroscopes used by cardiologists to properly position the device in the patient’s vasculature — were incremental when compared with the theoretical improvements of the Absorb BVS. Nevertheless, on the strength of these improvements, Boston Scientific has made significant inroads into the-bread and-butter DES market. Over the course of 2016, the SYNERGY overtook Abbott Vascular’s flagship DES, the XIENCE, previously the market leader in that segment.

All of this serves as a cautionary tale: Abbott’s focus on pushing the more revolutionary Absorb product may have diverted resources from making more prosaic improvements to the XIENCE, improvements that may have allowed Abbott Vascular to hold share against Boston Scientific’s SYNERGY. Nonetheless, Abbott recently acquired CE mark approval for its next-generation XIENCE product, the XIENCE Sierra. With the Absorb mothballed, it seems likely the company will begin a period of clawing back traditional DES market share from its main competitors on the back of such product improvements.

Despite this setback and the major manufacturers’ renewed focus on the DES market, there remain smaller players innovating in the BVS category. Elixir Medical originally secured CE mark approval for its DESsolve BVS in 201312 and, in May 2017, demonstrated the DESsolve’s success as a bioresorbable stent with low complication rates13. Other companies, such as Reva Medical and Amaranth Medical, are at various stages in commercializing their own BVS technologies.

Given the small size of the remaining players in the BVS market, we predict that one or more of these players will be acquired by the larger DES manufacturers (Abbott Vascular, Boston Scientific, or Medtronic) should they demonstrate positive outcome data in current or planned clinical trials. Although it is too early to forecast the eventual adoption rate of BVS and resulting market values, further attempts to commercialize BVS products in coming years seem all but assured.

Renal Denervation

Approximately 10-20 percent of the general hypertensive population suffers from resistant hypertension6, a form of hypertension where the patient’s systolic blood pressure remains over 140 mmHg, despite being treated with three or more anti-hypertensive medications. Renal denervation has emerged as a potentially ground-breaking solution for the untreated hypertensive population, holding out the promise of reducing the global burden of heart disease and stroke.

Medtronic’s Symplicity HTN-3 clinical trial was the largest, most rigorously designed study conducted on renal denervation for treatment-resistant hypertension, including blinding and sham treatment in the control group3. While the industry eagerly looked forward to the trial’s results, their release led to major disappointment and a change to the global renal denervation market in 2014.

Early that year, Medtronic revealed that, despite meeting its primary safety endpoint, the Symplicity HTN-3 clinical trial did not meet its primary or secondary efficacy endpoints. Although patients receiving renal denervation treatment had a large decrease in blood pressure, this was not statistically significant from the sham control group, who also showed a drop in blood pressure. This raised the question of why patients with resistant hypertension suddenly saw a drop in blood pressure, and whether they truly had resistant hypertension in the first place.

It was noted that several factors may have contributed to the efficacy results, despite the rigorous study design. In particular, unintended effects were present in both arms on patient medication compliance1, and more fundamental questions existed regarding whether the renal nerve actually was denervated in most patients (and how many nerves needed to be denervated before a patient’s blood pressure decreases)3.

These results forced the entire renal denervation industry to reevaluate its clinical trial designs, as well as pause any sales and marketing efforts. Currently, only a select number of countries in Europe have approved renal denervation devices for commercial use. In addition, companies have terminated on-going clinical trials and stopped commercialization in countries such as the U.K. and Australia. Smaller companies that entered this industry with high hopes and devices in development have abandoned their research altogether.

Following the industry downturn in 2014, the buzz around renal denervation devices remained fairly quiet, despite some ongoing research and development. However, the conversation has since reignited, led by clinical trials that learned from the failure of Symplicity HTN-3. The SPYRAL HTN-OFF MED trial aimed to “provide biologic proof of principle for the efficacy of renal denervation”9, where the trial included patients with uncontrolled hypertension who had not taken anti-hypertensive medications at least four weeks prior to randomization. Interim results showed that, with the new procedural approach and non-confounding measures, the reductions in all blood pressure measurements within the renal denervation arm compared to the sham arm were statistically significant2. Additionally, in August 2017, ReCor Medical added another $12 million for the trial of its Paradise renal denervation device7.

We believe renal denervation will make a comeback in the near future, potentially with devices released in major markets by 2018. In 2015, regulatory approval was given to several markets, including Brazil, Canada, Mexico, Russia, and several European countries, though the device was only marketed in a subset of these countries. As a result of successful clinical trials, we expect renal denervation devices to be present in 15 major markets across the world by 2022, with the largest markets being U.S., Germany, and France.

Since the market is still in its infancy and will depend on successful clinical trial results, three scenarios can be envisioned, based on different assumed adoption rates. The low-level adoption scenario assumes that clinical trial analysis and results will take some time to be published and, in combination with industry apprehension stemming from the HTN-3 trial, results in slow growth and market adoption. In this model, the global market is poised to hit approximately $400 million by 2022, growing at a CAGR of 33 percent.

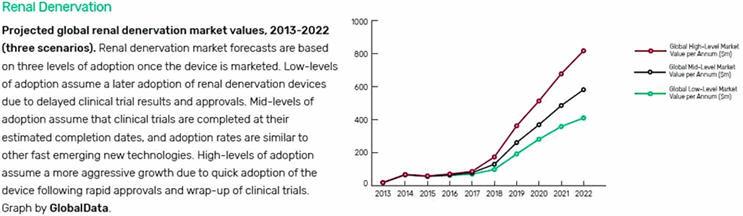

Projected global renal denervation market values, 2013-2022 (three scenarios). Renal denervation market forecasts are based on three levels of adoption once the device is marketed. Low-levels of adoption assume a later adoption of renal denervation devices due to delayed clinical trial results and approvals. Mid-levels of adoption assume that clinical trials are completed at their estimated completion dates, and adoption rates are similar to other fast emerging new technologies. High-levels of adoption assume a more aggressive growth due to quick adoption of the device following rapid approvals and wrap-up of clinical trials. Graph by GlobalData.

The high-level adoption assumes that clinical trials are successful and approval is rapid, where adoption and re-adoption occurs at an aggressive speed. Major markets, particularly the U.S., will try to speed up the process to gain a critical position in the fast-growing market. At a high-level adoption, the global market would grow at a CAGR of 45 percent and surpass $800 million in revenue by 2022.

Lastly, the mid-level adoption model forecasts the most likely scenario if clinical trials finish on time and results are published in a timely manner. It assumes that re-adoption will occur in markets that already have approval and other major markets will be in the process of gaining regulatory approval. The device will follow a growth trend similar to that of new and fast-emerging technology. The mid-level adoption model forecasts the renal denervation market to grow at a CAGR of 40 percent, reaching a market value of $580 million in 2022.

Despite the disappointing results from Medtronic’s clinical trial, there still is hope in the renal denervation market. This is because the possibility of renal denervation decreasing blood pressure has not yet been disproved, and earlier evidence from animal and human studies suggests the treatment will work (for example, significant drops in blood pressure were observed from surgical denervation of the kidney as early as the 1920s). Therefore, this innovative intervention may still prove efficacious in treating drug-resistant hypertension.

Conclusion

As these examples illustrate, innovation in medical devices is risky, given the enormous expense involved in developing new technologies and in running the clinical trials necessary to bring them to market. Despite the high stakes, companies invested in medical device growth will continue to take calculated risks in key categories.

Despite these cautionary tales, it is important to appreciate the contribution that even failed technological innovation has on the longer-term prospects for improved medical devices. In the case of renal denervation, a great deal of post-hoc analysis of the failed SYMPLICITY HTN-3 trial has led to the sort of hypothesis-generation required to design better devices and study protocols (if renal denervation is ultimately successfully commercialized, it will be due to the lessons learned from this trial).

In the BVS segment, the more common complaints raised about the Absorb (for example, its high strut thickness and lack of ‘trackability’) are a principal focus of the remaining BVS players’ R&D efforts, which focus on thinner struts and easier deployment. Although the companies that initially fail in developing a certain technology are not always beneficiaries when the technology is ultimately successful, such early failures often do pay off down the road for the market as a whole, and ultimately lead to improved human health.

About The Authors

Alexander Marsolais, PhD, joined GlobalData in 2016 on the medical consulting team, and specializes in market assessment and forecasting, market access, and strategy. His work includes both quantitative and qualitative market research across a wide range of medical specialties, including cardiovascular medicine, medical diagnostics, orthopedics, and general surgical procedures. He also advises on market research methodology on GlobalData’s syndicated research projects. Prior to joining GlobalData, Alexander worked as a Senior Analyst at Decision Resources Group and developed an expertise in cardiovascular medicine while authoring reports on diverse markets in the US, Europe and Asia. Alexander holds a PhD in Biochemistry from the University of Toronto, with a research focus in the area of cell biology and gene expression.

Sheryl Tang is a Medical Devices Analyst at GlobalData Healthcare with a focus on Cardiovascular devices. Her work includes the collection and analysis of quantitative and qualitative information to develop data products that forecast the characteristics of various cardiovascular device markets across the world. Sheryl’s research activities include speaking to industry leaders as well as incorporating real-world data into data products, enabling her to have an in-depth understanding of the market. Before joining GlobalData, Sheryl has had various experiences in public health including interning as a Community Health and Development analyst at Toronto Public Health. She has a Bachelor of Health Sciences from Western University and recently received a Masters of Public Health, which provides her with a strong understanding of the Canadian healthcare system and analysis of epidemiology data.

James Spencer is a Medical Devices Analyst at GlobalData in Toronto. Prior to joining GlobalData, James worked as an R&D engineer in the medical devices industry, prototyping and developing novel surgical prototypes, while improving efficiencies in production methodologies and workflows. He received his BASc in Biomedical Engineering from the University of Toronto, where he worked in Robotics labs to develop software for the healthcare industry.

References:

- European Hospital (2014). Renal denervation on razor`s edge ahead of trial results. European Hospital. Available from: http://www.healthcare-in-europe.com/en/article/11653-renaldenervation-on-razor-s-edge-ahead-of-trial-results.html

- European Society of Cardiology. Renal denervation lowers blood pressure in hypertensive patients not taking medication (SPYTAL HTN-OFF MED). Available from: https://www.escardio.org/The-ESC/Press-Office/Press-releases/renal-denervation-lowers-blood-pressure-in-hypertensive-patients-not-taking-medication

- Fornell D. (2014). The future of renal denervation following the failed SYMPLICITY HTN-3 Trial. Diagnostic and Interventional Cardiology. Available from: https://www.dicardiology.com/article/future-renal-denervation-following-failed-symplicity-htn-3-trial

- GlobalData. (2016). MediPoint: Renal Denervation – Global Analysis and Market Forecasts

- Gupta AK (2010). Racial differences in response to antihypertensive therapy: Does one size fits all? International Journal of Preventative Medicine; 1(4): 217-219. Available from: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3075515/

- Myat A, et al. (2012). Clinical Review: Resistant Hypertension. The British Medical Journal; 345:7473. Available from: http://www.bmj.com/content/345/bmj.e7473

- ReCor Medical. (2017). ReCor Medical adds another $12m for trial of Paradise renal denervation device. Available from: http://www.recormedical.com/blog/2017/08/28/recor-medical-adds-another-12m-for-trial-of-paradise-renal-denervation-device/

- Santiapillai GR and Ferro A (2014). Renal denervation as an option for the management of hypertension. The Journal of Biomedical Research; 28(1): 18-24. Available from: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3904171/

- Wendling P. (2017). SPYRAL HTN-OFF MED: Reopens renal denervation conversation. Medscape. Available from: https://www.medscape.com/viewarticle/884917

- Serruys PW, Chevalier B, Sotomi Y, et al. Comparison of an everolimus-eluting bioresorbable scaffold with an everolimus-eluting metallic stent for the treatment of coronary artery stenosis (ABSORB II): a 3-year, randomized, controlled, single-blind, multicenter trial. Lancet. 2016; Epub ahead of print.

- O'Riordan, Michael. “FDA Warns of Risk of Major Adverse Cardiac Events With Absorb BVS.”TCTMD.com, Tctmd, 18 Mar. 2017, www.tctmd.com/news/fda-warns-risk-major-adverse-cardiac-events-absorb-bvs.

- “Press Releases.” Elixir Medical Corporation - Press Releases, Elixir Medical, 15 May 2013, elixirmedical.com/index.php?mact=News%2Ccntnt01%2Cdetail%2C0&cntnt01articleid=18&cntnt01origid=69&cntnt01returnid=69.

- “Elixir Medical Corporation Announces Outstanding 5-Year Clinical Data for CE Mark-approved DESolve® Novolimus Eluting Bioresorbable Coronary Scaffold System” Elixir Medical Corporation - Press Releases Template, Elixir Medical, 17 May 2017, elixirmedical.com/index.php?mact=News%2Ccntnt01%2Cdetail%2C0&cntnt01articleid=46&cntnt01origid=69&cntnt01returnid=110.