U.S. Ultrasound Market Driven By Growth In POC Segment, Use Of High-End Equipment

By Kamran Zamanian, Ph.D., CEO, and Lucas Parker, senior research analyst, iData Research Inc.

The market for ultrasound equipment has been growing steadily and is expected to continue growing for years to come. The two largest segments of the overall ultrasound equipment market in 2014 were cardiology and radiology segments. Radiology was the first area to use ultrasound equipment intensively. Due to the large number of important applications, cardiology has also become a traditional setting for the use of ultrasound devices. These respective segments each accounted for over 25% of the overall market.

Cardiology and radiology are highly saturated segments of the ultrasound equipment market. However, due to advances in 3D and 4D imaging, as well as elastography and combined MRI/ultrasound imaging techniques, growth rates in these markets are expected to remain in the mid-single digits until at least 2020.

Point-Of-Care Represents Fastest Growing Segment

Point-of-care (POC) applications represented the fastest growing segment of the ultrasound equipment market in 2014, and will continue to outstrip other segments over the next decade.

The POC ultrasound equipment market comprises a large number of subsegments corresponding to different medical service delivery sites. Examples include emergency department, critical care, anesthesiology and musculoskeletal applications. These areas of medical service delivery have not traditionally relied on ultrasound for their diagnostic evaluations. However, due to technological improvements and reductions in the cost of ultrasound equipment, these areas are rapidly adopting ultrasound as a tool for diagnostic and guidance procedures.

Anesthesiology and musculoskeletal are expected to be the two fastest growing segments of the overall POC ultrasound equipment market. In these settings, physicians are using ultrasound to improve the accuracy of needle placement procedures and to replace costly radiation-based imaging techniques with real-time, cost-effective ultrasound imaging.

The U.S. market for POC ultrasound systems was not saturated in 2014. There are many healthcare facilities that do not own POC ultrasound systems, and those that do are likely to purchase additional units in the future. Additional units are especially useful in hospital emergency rooms where multiple patients require treatment simultaneously.

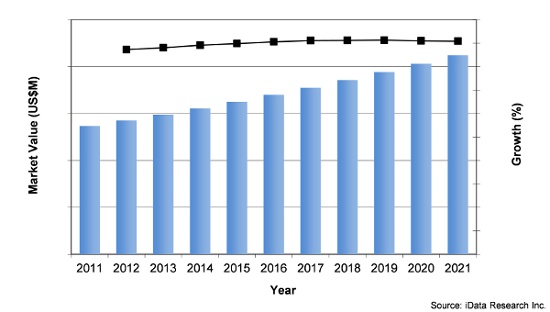

Ultrasound Equipment Market, U.S., 2011 – 2021

Rising Popularity Of TTE Puts Upward Pressure On Prices

In recent decades, the practice of ultrasound for cardiology applications has been dramatically affected by the invention of transesophageal echocardiography (TEE). In contrast to transthoracic echocardiography (TTE), during which ultrasound probes are placed noninvasively on the patient’s chest, TEE is an invasive procedure that involves the insertion of an endoscope into the patient’s esophagus. The endoscope is equipped with a small transducer. These procedures are frequently performed in the operating room under general.

The growing popularity of TEE procedures is putting upward pressure on prices in this otherwise stable replacement market. TEE probes are extremely expensive relative to other ultrasound probes, typically adding around $29,000 to the price of a machine. As TEE becomes more popular, and cardiology departments purchase TEE probes along with other standard cardiology ultrasound equipment, prices in the cardiology market will increase.

We maintain a database on procedure volumes for specific procedures at the national, state, hospital, and physician level. Procedure volume data reveals that TEE procedures have increased by 18% over the past four years. During the same period, TTE procedures grew by only 4%.

Dual-Probe Handheld System Helps GE Shore Up Already Dominant Position

he market for medical ultrasound imaging equipment is highly saturated, with markets for traditional cardiology and general imaging systems being controlled primarily by two or three top competitors. However, after Sonosite came out with the first hand-carried ultrasound system and took over a large piece of the POC ultrasound market, there has been more volatility in the overall competitive landscape. Today, the POC ultrasound market has become crowded, with many of the largest ultrasound and medical imaging companies having developed products in this market segment.

One highly successful product has been the Vscan from GE Healthcare. Vscan differs from many of the handheld devices on the market in that it is equipped with a linear probe that operates at higher frequency and allows for imaging of superficial structures. This aspect of the device means that in theory it could be used for vascular access, although this application remains limited. Phased array capabilities for deeper structure imaging are also included in the system’s dual-probe transducer. In contrast, competing devices are only designed for deep structure imaging with the associated phased array transducers.

About iData Research

iData Research (www.idataresearch.com) is an international market research and consulting group focused on providing market intelligence for medical device and pharmaceutical companies. iData covers research in: diabetes drugs, diabetes devices, pharmaceuticals, anesthesiology, wound management, orthopedics, cardiovascular, ophthalmics, endoscopy, gynecology, urology, and more.

About Procedure Tracker

Procedure number data is available from iData’s Procedure Tracker service, which allows subscribers to define and analyze procedure data segmented by state, region, hospital, surgery center, and physician. A customizable dashboard sorts procedure data for further analysis and research.

About The Authors

Lucas Parker is a senior research aalyst at iData Research. He is Procedure Tracker’s lead designing analyst, specializing in data extraction protocols and the development of procedure-based forecast models for markets in ultrasound, laproscopic medicine, and interventional cardiology. He can be reached at lucasp@idataresearch.net or on LinkedIn.

Kamran Zamanian, Ph.D., is president, CEO, and a founding partner of iData Research. He has spent over 20 years working in the market research industry.