US Market Trends For Computer-Assisted & Robotics-Assisted Surgery

By Devon Philpott and Kamran Zamanian, iData Research

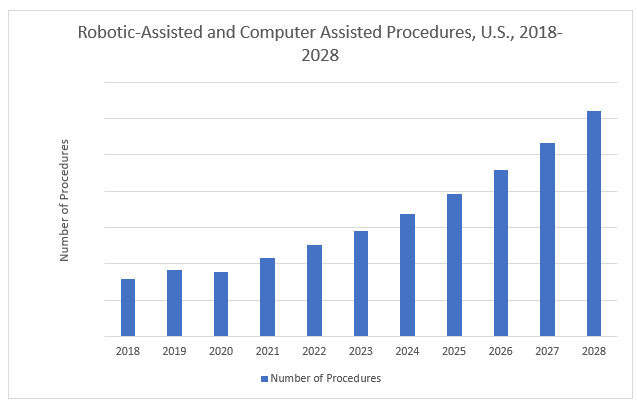

In the medical industry, adoption of new cutting-edge technology is slow compared to other industries, such as the automotive industry.1 Computer-assisted and robotic-assisted surgery (CAS and RAS, respectively) have been around for decades, yet a small percentage of procedures performed take advantage of the innovative solutions available on the market today. In coming years, the number of procedures using robotics and surgical navigation is predicted to increase at a double-digit rate year over year to reach over 6 million procedures by 2028.2 This rise in CAS and RAS can be attributed to the predicted increase in the utilization of navigation systems and robotic devices as more companies launch new or next-generation systems for assisted surgery.

In the medical industry, adoption of new cutting-edge technology is slow compared to other industries, such as the automotive industry.1 Computer-assisted and robotic-assisted surgery (CAS and RAS, respectively) have been around for decades, yet a small percentage of procedures performed take advantage of the innovative solutions available on the market today. In coming years, the number of procedures using robotics and surgical navigation is predicted to increase at a double-digit rate year over year to reach over 6 million procedures by 2028.2 This rise in CAS and RAS can be attributed to the predicted increase in the utilization of navigation systems and robotic devices as more companies launch new or next-generation systems for assisted surgery.

Reasons For Slow CAS And RAS Adoption

Some argue that using CAS and RAS is not worth the time and monetary investment, as using this technology often increases procedure planning time and reduces the number of procedures a facility can complete in a certain time frame.3 However, more studies have come out in recent years that highlight the clinical benefits of using CAS or RAS compared to unassisted surgeries. For example, it has been found that using navigation for total hip arthroplasty (THA) procedures significantly reduces hip dislocations and the need for future revision surgeries compared to unguided surgeries.4,5 Other studies have shown that using RAS can drastically reduce recovery times, allowing patients to spend less time in the hospital post-operation.6,7 As more studies like this are published, adoption of CAS and RAS is expected to increase.

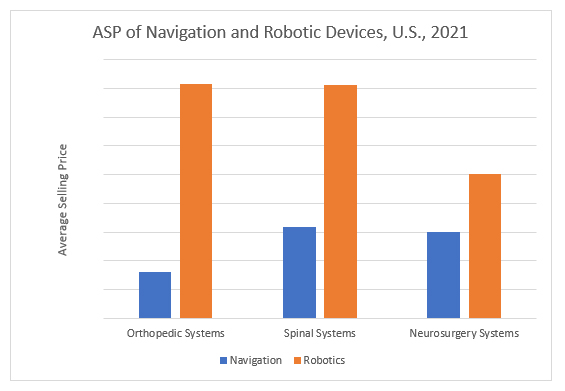

An exception to these doubts is neurosurgery procedures; it is considered to be the standard of care that neurosurgeries use a navigation system. Because of this, the neurosurgery navigation system market has the highest adoption rate and poses a challenge to companies attempting to penetrate the market by offering state-of-the-art robotic systems. In addition to the slow adoption of new technology, robotic solutions tend to be much more costly than navigation devices, some of which have an average selling price (ASP) upwards of $1 million for one robot while navigation systems tend to be a fraction of that cost.2 However, some companies, such as Brainlab, have developed affordable robotic solutions with pricing that is competitive with navigation systems on the market.

Recent Advancements To CAS And RAS

Since 2018, the FDA has made several approvals in the U.S. robotics and surgical navigation market, including clearances for devices as well as updated software modules. The companies that were granted clearance for their navigation and robotics products include, but are not limited to, Auris Health, Brainlab, DePuy Synthes, Intuitive Surgical, Medtronic, Smith & Nephew, and Zimmer Biomet. These companies are staying up to date with market trends as they have all developed robots for procedures with the highest compound annual growth rate over the forecast period, according to the iData Research report.2 Brainlab, Medtronic, and Zimmer Biomet have come up with robotic solutions for neurosurgery, while DePuy Synthes, Smith & Nephew, and Zimmer Biomet have developed new robots to perform orthopedic procedures.

The minimally invasive surgery (MIS) segment of the robotic-assisted surgery market is the largest, with approximately 85% of all robotic procedures performed in 2021 being minimally invasive.2 The robotic-assisted MIS segment has been dominated by Intuitive Surgical; however, more companies have entered the market, looking to compete with Intuitive’s da Vinci system. Auris Health and Medtronic have both released robotic solutions for MIS alongside several other competitors looking to chip away at Intuitive Surgical’s share of the market. These product releases are anticipated to help drive robotic procedure volume as these companies are well established in the medical device industry.

Of all navigated orthopedic procedures, THA has the lowest adoption compared to total or partial knee arthroplasties.2 However, computer-assisted THA procedures are expected to increase at the fastest rate due to the development of fluoroscopy-based navigation systems. These systems have gained immense popularity over the last decade or so, which in turn led to an increase in THA procedures performed from a direct anterior approach.8 Although most navigated orthopedic procedures done in 2021 were knee procedures, those procedures are expected to exhibit a slower growth rate over the forecast period.2

Current CAS And RAS Adoption

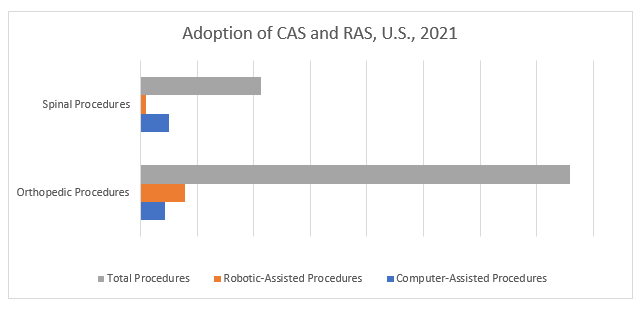

Another major factor that impacts the adoption rate of CAS and RAS is the procedure type. For minimally invasive robotics, urological procedures have the highest robotic penetration while cardiac procedures have the lowest adoption rate.2 While there is a small margin of error for all surgeries, there is more caution taken for procedures that involve vital organs such as the heart, hence the low adoption rate. For spinal surgery, the adoption of CAS was nearly sevenfold higher than that of RAS in 2021.2 Interestingly, the opposite is seen for orthopedic surgery, where RAS adoption was over two times higher than CAS in 2021.2 The difference in trends seen for orthopedic and spinal surgeries is likely due to the several new robotic orthopedic systems released recently, such as DePuy Synthes’ VELYS Robotic-Assisted Solution.

Conclusion

There is no doubt that as technology advances across the globe, more surgeries will be performed that make use of the updated technological advancements. With the release of long-term impact studies, new product launches, and training programs, more patients and surgeons will feel comfortable opting for a computer-assisted or robotic-assisted approach over an unguided approach for their surgery. An increase in procedure volume is coupled with an increase in disposable surgical costs, driving the overall robotics and surgical navigation market in the United States.

References

- Shaw B, Chisholm O. Creeping Through the Backdoor: Disruption in Medicine and Health. Front Pharmacol. 2020;11:818. doi:10.3389/fphar.2020.00818

- iData Research Inc. U.S. Surgical Robotics and Navigation Market – 2022. Published June 17, 2022. Accessed June 17, 2022. [URL].

- Bakalar N. Are robotic surgeries really better? The New York Times. https://www.nytimes.com/2021/08/16/well/live/robotic-surgery-benefits.html. Published August 16, 2021. Accessed May 13, 2022.

- Agarwal S, Eckhard L, Walter WL, et al. The use of computer navigation in total hip arthroplasty is associated with a reduced rate of revision for dislocation: a study of 6,912 navigated THA procedures from the Australian Orthopaedic Association National Joint Replacement Registry. Journal of Bone and Joint Surgery. 2021;103(20):1900-1905. doi:10.2106/JBJS.20.00950

- Sharma AK, Cizmic Z, Carroll KM, et al. Computer navigation for revision total hip arthroplasty reduces dislocation rates. JOIO. Published online February 24, 2022. doi:10.1007/s43465-022-00606-7

- Using the da Vinci robot for minimally invasive surgery. Accessed May 13, 2022. https://www.adventisthealth.org/blog/2022/february/using-the-da-vinci-robot-for-minimally-invasive-/

- Ali M, Kamson A, Yoo C, Singh I, Ferguson C, Dahl R. Early superior clinical outcomes in robotic-assisted TKA compared to conventional TKA in the same patient: a comparative analysis. J Knee Surg. Published online February 18, 2022. doi:10.1055/s-0042-1743232

- Werner JA, Schwarz J, Werner LA. The evolution of anterior total hip arthroplasty: the past, present, and future. Bulletin of the NYU Hospital for Joint Diseases. 2021;79(1):51-58. Accessed May 13, 2022. https://go.gale.com/ps/i.do?p=HRCA&sw=w&issn=19369719&v=2.1&it=r&id=GALE%7CA654815391&sid=googleScholar&linkaccess=abs

About The Authors:

Devon Philpott is a research analyst at iData Research. She develops and composes syndicated research projects regarding the medical device industry, publishing the U.S. Robotic and Surgical Navigation report series.

Kamran Zamanian, Ph.D., is CEO and founding partner of iData Research. He has spent over 25 years working in the market research industry with a dedication to the study of medical devices used in the health of patients all over the globe.

About iData Research

For 17 years, iData Research has been a strong advocate for data-driven decision-making within the global medical device, dental, and pharmaceutical industries. By providing custom research and consulting solutions, iData empowers its clients to trust the source of data and make important strategic decisions with confidence.